With the country being known as one of the leading financial hubs globally, taxation here in Singapore is quite favourable. The famed Lion City has one of the best business environments where you can find tax-friendly policies, a competitive workforce, and a stable government. Singapore is consistently ranked high in the “Ease of Doing Business Index” published by the World Bank. In 2020, it ranked second behind New Zealand.

With robust infrastructure and a healthy economic landscape, Singapore has attracted investors to put their wealth in the Merlion city. Singapore’s assets under management (AUM) keep increasing. In 2019, its AUM grew 15.6% to reach S$4.0 trillion.

That figure ballooned to S$4.7 trillion a year later, signalling a 17% increase year-on-year.

The Monetary Authority of Singapore (MAS) oversees and regulates financial institutions in Singapore. MAS has outlined the regulations for all companies operating in the fund manager space with the Securities and Futures Act (SFA).

Types of Fund Management in Singapore

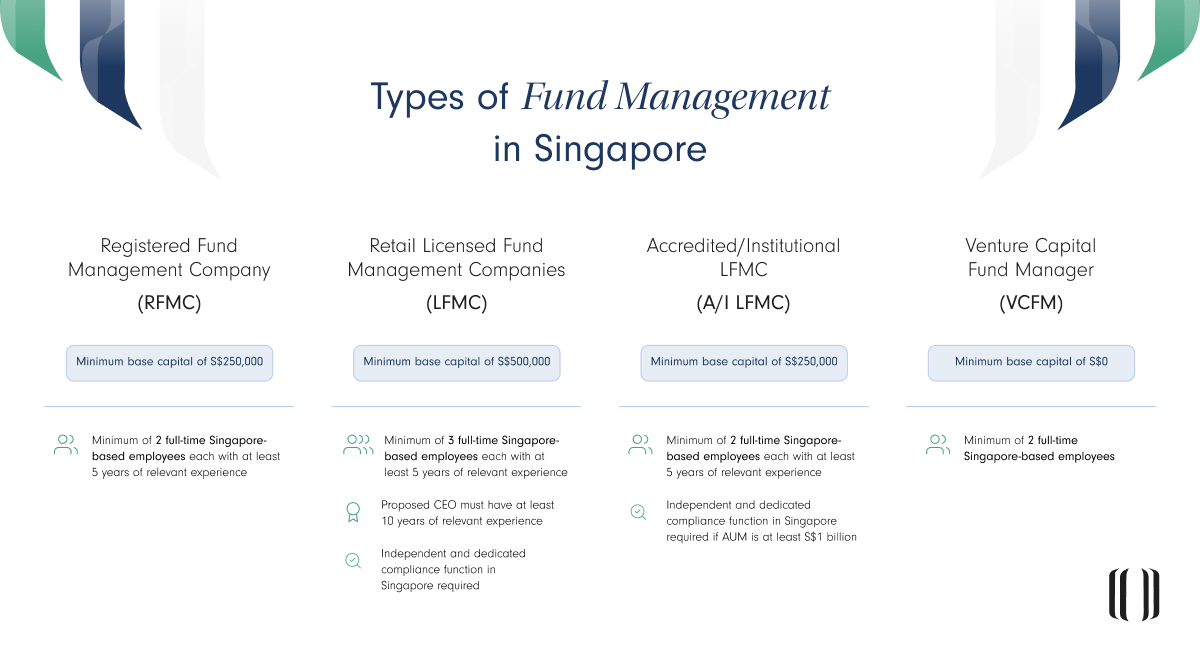

In conducting regulated fund management activities in Singapore, a company must be registered with the Monetary Authority of Singapore MAS or hold a Capital Markets Services (CMS) licence to operate here. There are four types of fund management structures to choose from, which are:

Registered Fund Management Company (RFMC)

A company that may have up to 30 accredited and institutional investors with a total of S$250 million in assets under management.

Retail Licensed Fund Management Companies (LFMC)

As the name suggests, this type of company conducts fund management with all kinds of investors, including retail or individual investors.

Accredited/Institutional LFMC (A/I LFMC)

This type of company only manages funds for accredited and institutional investors.

Venture Capital Fund Manager (VCFM)

Refers to management companies that only manage venture capital funds, meaning that it’s primarily invested in startups. This type of company is also only for accredited and institutional investors.

The capital needed to establish the fund management depends on the type. RFMC and A/I LFMC require S$250,000, whereas VCFM and RFMC need S$0 and S$500,000, respectively. When it comes to requirements in appointing a director, each type has a different requirement as follows:

-

- RFMC and A/I LFMC

At least two directors possess a minimum of five years of relevant experience. One should at least be an executive and full-time resident in Singapore.

- RFMC and A/I LFMC

-

- Retail LFMC

At least two directors possess more than five years of relevant experience. One should at least have ten years of experience and be a full-time resident in Singapore.

- Retail LFMC

-

- VCFM

At least two directors whose experience in fund management may be less than five years.

- VCFM

Once you have chosen the type of business you want to engage in and the right people to manage the business, MAS will assess your application based on the following:

-

- Fitness and propriety of the applicant, its shareholders and directors.

-

- Track record and fund management expertise of the applicant and its parent company or major shareholders.

-

- Ability to meet the minimum financial requirements prescribed under the SFA.

-

- Strength of internal risk management and compliance systems.

-

- Business model/ plans and projections and the associated risks.

Available Exemptions for Fund Managers

After knowing the different types of fund management available, you may think that taxation in Singapore only applies to companies with a local presence. But, this is not necessarily the case. Conceptually, funds managed by fund managers in Singapore may be considered to establish a taxable presence in Singapore, even if the company they worked for is incorporated elsewhere.

However, Singapore offers an attractive tax regime for its growing fund management industry. There are several regulations that fund managers have to comply with in Singapore. And depending on the size and funds managed, there are several tax incentives for fund managers they can take into consideration:

Onshore Fund Tax Incentive Scheme (13R)

This type of tax incentive for fund managers is specially designed for companies that have a local footprint in Singapore with assets or funds managed by a fund manager who lives in Singapore.

The company must have investors composed of individual investors, non-resident corporate investors, or Singaporean corporate investors who own no more than 30% of the fund. The percentage increases to 50% when there are more than ten investors. It’s prohibited for the fund to be wholly owned by Singaporeans. Fulfilling such requirements is necessary to qualify for the tax exemption.

Additionally, the company must spend at least S$200,000 annually on local business spending, including management fees, remuneration, and other operating costs. The total fund managed has no limit or restrictions. Still, the fund manager is obligated to declare to the Inland Revenue of Authority Singapore (IRAS) and produce a financial statement to investors annually.

Enhanced-Tier Fund Tax Incentive Scheme (13X)

While this tax incentive for fund managers shares some similarities to the 13R tax scheme, such as the requirement of having a minimum local business spending of S$200,000 annually, the 13X scheme has several differences. The first is the type of investor that can join the fund is not restricted. Everyone from all walks of life can invest in the fund, so if the fund ends up being 100% owned by Singaporeans, MAS will not flag it.

The other difference is the amount of funds being managed. While the 13R scheme has no minimum on the size of the fund, the 13X scheme needs a minimum of S$50 million to qualify for the exemption. Fund managers also have no obligation to give financial statements to investors annually, though they are still required to report to IRAS.

Offshore Fund Scheme (13CA)

This tax scheme is designed for funds not based in Singapore but managed by a Singaporean fund manager based in the ‘melting pot’ city. This scheme shares a few similarities with both tax schemes explained above. The type of investors managed by the business must be the same as that tax scheme 13R. Having a local footprint is not necessary to qualify for the scheme.

As the fund is based overseas and not in Singapore, fund managers have no obligation to deal with IRAS, like the 13X tax scheme, or have a local business spending minimum to get tax exemptions. Although this tax incentive for the fund manager applies, they are still obliged to send investors annual financial statements.

Remember that these three tax exemptions for fund managers only apply to Specified Income from Designated Investments, covering a wide range of investments, including stocks, shares, bonds, securities and derivatives. The main kind of investment that’s not exempt is real estate in Singapore.

Tax Incentives For Fund Managers in Singapore

Generally, investors pay fees to fund managers to provide advisory and management services to the fund. The fees paid are subject to a tax rate of 17%. The figure is cut down to 8.5% for the first S$ 200,000.

The standard 17% tax rate could be lowered to 10% if the fund manager fulfilled certain criteria set in The Financial Sector Incentive for fund managers (FSI-FM). This happens due to the programme’s objective to promote and encourage fund management activities in Singapore.

Fund managers need to adhere to the following three criteria to get the concessionary 10% tax rate:

-

- Fund managers must hold a Capital Markets Services (CMS) licence.

-

- Have a minimum of S$250 million in assets under management (AUM).

-

- Have at least three experienced investment professionals such as portfolio managers, research analysts, and traders.

Moreover, there’s no capital gain tax in Singapore, meaning that if the fund manager sold his investments, whether in stocks or bonds, he or she will not have to pay tax to the government, giving investors more profits and for them too, if they invest personally with their earnings.

Foreign income that’s not earned or transferred to Singapore is most likely tax-free. However, if you’re a Singaporean company or a resident, your foreign transferred income to your bank will most likely be taxed, as outlined above. Only businesses and individuals that comply with the existing regulations can qualify as non-taxable. Hiring a professional service like Lanturn to guide and assist you on foreign income tax matters can make the process much easier.

Work with us

As one of the leading technology firms that provide end-to-end financial services and solutions for businesses, Lanturn has a proven track record in fulfilling clients’ needs. This includes dealing with the Singaporean tax system that some may find complicated, especially as the government continuously updates policies to ensure they are working well.

Our certified and experienced team is ready to help you ease the complexities of tax filings, incorporate a management fund business, or even startup fundraising.

Want to deal with your financial needs hassle-free? Contact us now.